UK Share Investors: HMRC Tax Rules for Capital Gains, ERI, Dividends and Interest

For UK private investors holding shares, ETFs, investment trusts or funds outside an ISA or SIPP, tax reporting can become increasingly complex—especially when you start selling investments, receiving dividends or holding offshore reporting funds.

UK HMRC Shares and Capital Gains Tax helpsheet HS284

This guide covers:

- Capital Gains Tax (CGT) annual allowances

- CGT tax rates

- Excess Reported Income (ERI) on offshore ETFs/funds

- Dividends and broker tax reports

- Interest on cash

1. Capital Gains Tax (CGT) Annual Allowance

UK private individuals receive an Annual Exempt Amount (AEA) for capital gains. This is the amount of gains you can make in a tax year before CGT becomes payable.

For share investors, this applies to gains from:

- Individual shares

- ETFs

- Investment trusts

- Unit trusts and OEICs

- Offshore reporting funds

Official HMRC guidance:

HMRC Capital Gains Tax rates and allowances

HMRC reference: SA108 Capital Gains Tax summary form and notes.

HMRC UK Capital Gains share matching rules

The order of priority for matching share buys to share sells (including FIFO)

- Same-Day Rule

- Shares sold are matched first against any shares of the same class acquired on the exact same calendar day.

- 30-Day Rule (Bed & Breakfasting) with FIFO

- Remaining sold shares are matched against acquisitions made within the 30 calendar days following the day of disposal.

- The FIFO Rule: If you make multiple purchases within this 30-day window, matching occurs chronologically. The earliest purchase inside the window is matched first until exhausted, before moving to the next chronological purchase.

- Section 104 Pool

- Any remaining sold shares that cannot be matched by steps 1 or 2 are matched against the average cost of the Section 104 Pool (the collective pool of all shares held prior to the day of sale).

CGT Annual Allowance (Private Individuals)

| Tax Year | Annual CGT Allowance |

|---|---|

| 2016/17 | £11,100 |

| 2017/18 | £11,300 |

| 2018/19 | £11,700 |

| 2019/20 | £12,000 |

| 2020/21 | £12,300 |

| 2021/22 | £12,300 |

| 2022/23 | £12,300 |

| 2023/24 | £6,000 |

| 2024/25 | £3,000 |

| 2025/26 | £3,000 |

After several years of stability, the allowance was significantly reduced from April 2023 onward.

2. Capital Gains Tax Rates on Shares

For most share disposals, CGT depends on whether your taxable income keeps you in the basic-rate band or higher-rate band.

CGT Rates for Shares, ETFs and Funds

| Tax Year | Basic Rate Taxpayer | Higher Rate Taxpayer | Notes |

|---|---|---|---|

| 2021/22 | 10% | 20% | Standard rates |

| 2022/23 | 10% | 20% | Standard rates |

| 2023/24 | 10% | 20% | Standard rates |

| 2024/25 (6 Apr–29 Oct) | 10% | 20% | Before October Budget |

| 2024/25 (30 Oct–5 Apr) | 18% | 24% | After October Budget |

| 2025/26 | 18% | 24% | Current |

When calculating your CGT, you first deduct:

- Allowable purchase cost

- Trading costs (where allowable)

- Any previous ERI already taxed for the shares sold (if applicable)

- Annual CGT allowance (from total)

The remaining gain is then taxed at the appropriate rate by HMRC.

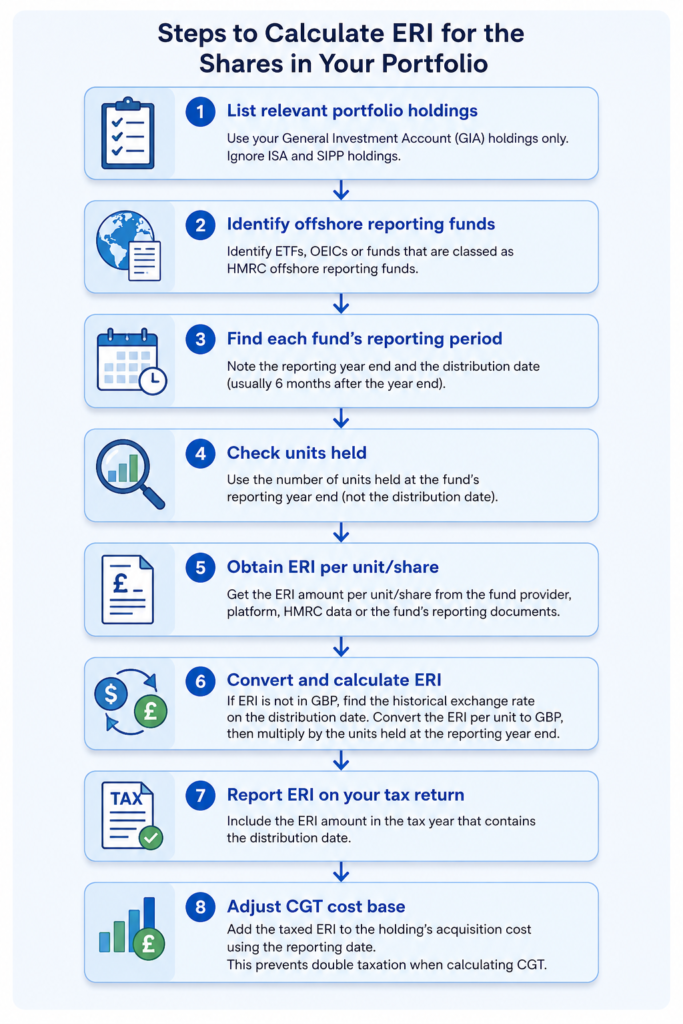

3. ERI (Excess Reported Income)

Many ETFs available to UK investors are offshore funds with UK reporting fund status, commonly domiciled in:

- Ireland

- Luxembourg

Examples include ETFs from:

- Vanguard

- BlackRock

- Invesco

These funds may retain income inside the fund rather than paying it out. That retained taxable income is called Excess Reported Income (ERI).

For most equity ETFs, ERI is usually treated as a notional overseas dividend for UK tax purposes.

However, ERI is not always dividend income. Some funds—particularly money market or cash-like funds—may classify the reportable income as an amount treated in the same way as interest for UK tax purposes, rather than dividend income. These amounts are still subject to income tax, but under interest rules rather than dividend rules.

So investors should always check the ETF’s Reportable Income document to confirm the exact tax treatment.

HMRC Reporting Funds List

HMRC publishes the official list of reporting funds here:

HMRC Offshore Funds List of Reporting Funds

This lets you verify:

- Whether your ETF had reporting fund status (lookup the ISIN)

- The dates reporting status applied to your particular share

Key ERI Dates

1. Reporting Period End Date

This is the ETF’s accounting year-end.

Example:

31 December 2025

If you held the ETF on this date, ERI may apply to you.

2. Fund Distribution Date

This is normally 6 months after the reporting period end.

Example:

Reporting period end = 31 Dec 2025

Distribution date = 30 Jun 2026

This is normally when the ERI becomes taxable for UK investors. It a notional distribution which you received on the distribution date (even if you no longer hold those shares).

Distributing vs Accumulating ETFs

A practical point many UK investors discover:

Distributing ETFs (“Dist”)

Distributing ETFs physically pay out their dividends.

Because the income has already been distributed, many distributing ETFs often report zero ERI or only a very small ERI in most years.

Accumulating ETFs (“Acc”)

Accumulating ETFs reinvest income inside the fund.

Because income is retained rather than paid out, accumulating ETFs often generate some notional ERI each year.

This creates additional tax administration in a General Investment Account (GIA), because:

- ERI may need declaring each year even though no cash was received

- ERI records must be kept for future CGT adjustments

For this reason, many UK investors prefer to hold distributing ETFs rather than accumulating ETFs in a GIA, because distributing ETFs often result in little or no ERI reporting.

Accumulating ETFs are often simpler inside ISAs or SIPPs, where ERI reporting is generally irrelevant.

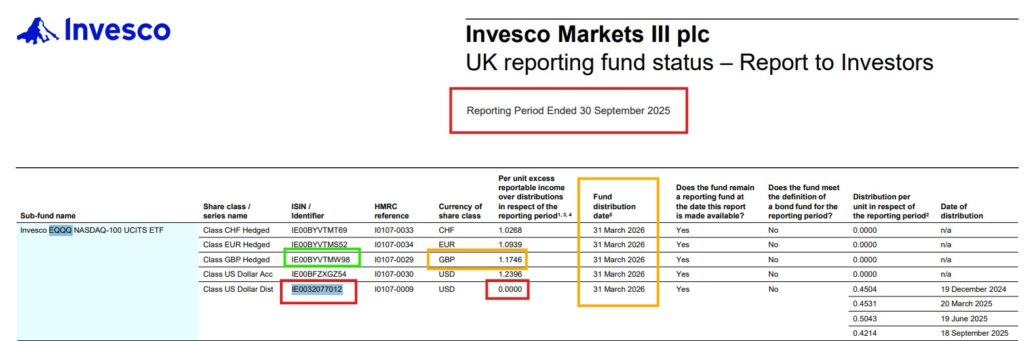

Example: Finding ERI for EQQQ

Suppose you hold:

Invesco EQQQ NASDAQ-100 UCITS ETF (dist.)

EQQQ is a distributing fund so the ERI would be expected to be 0 or very small (e.g. $0.04 per share). There are two common ways to find the ERI amount.

Method 1 — KPMG Reporting Fund Database

KPMG hosts a searchable database of reporting fund data:

KPMG Reporting Funds Database (free sign-in required – search using the ISIN number for best results)

Tip: Most broker sites will display the ISIN number if you look up the ticker symbol.

Steps:

- Register with KPMG for free investor access

- Search for EQQQ (or the ISIN for more accurate results)

- Open the correct share class (if only a few years are shown, it usually means the ERI was 0 for the missing years)

- Review the tax report

You will usually see:

- Reporting period

- Distribution amount

- Excess Reported Income per share (for that tax year)

- Distribution date

Method 2 — Provider Website

Many ETF providers publish reporting fund documents directly on their product pages.

For example:

Steps:

- Search for Invesco EQQQ NASDAQ-100 UCITS ETF

- Open the fund’s Documents or Literature section

- Find the Reportable Income document (sometimes called Reporting Fund Report) for the appropriate tax year or accounting period

- Open that report and locate:

- Reporting period end date

- Fund distribution date (always end of the month 6 months later)

- Excess Reported Income (ERI) per share/unit

That ERI per share is the amount you multiply by the number of shares you held on the reporting period end date.

ERI Calculation Example

Suppose:

You held 200 shares of Invesco EQGB NASDAQ-100 UCITS ETF (acc) on the Reporting Period End Date.

The Reportable Income document shows:

ERI = $0.85 per share

Total ERI:

200 × $0.85 = $170

Note that the distributing ETF EQQQ may have an ERI of 0 or a small amount such as $0.04 because in most years, the dividends are paid out to share holders as separate payments.

Foreign Currency Conversion

Most offshore ETFs report ERI in a foreign currency, commonly USD or EUR.

For UK tax reporting, the ERI must be converted into GBP using the exchange rate on the Fund Distribution Date.

It is the distribution date exchange rate—not the purchase date, reporting date or sale date—that should normally be used.

HMRC exchange rates can be found here:

Example

Suppose:

ERI = $170

Distribution date = 30 June 2026

Assume the GBP conversion on that date gives:

$170 = £136

It is £136 that is declared as taxable overseas dividend income on your UK tax return (assuming the fund classifies the ERI as dividend income).

The Reporting Date Rule (Very Important)

ERI only applies if you actually held the ETF on the fund’s Reporting Period End Date.

If you did NOT hold the ETF on the Reporting Period End Date

No ERI arises for that reporting period.

That means:

- No ERI income to declare

- No ERI cost adjustment for CGT

If you sold the ETF just before the Reporting Period End Date or bought the ETF just after the Reporting Period End Date, you were not a holder on that date, so no ERI applies for that reporting period.

If you DID hold the ETF on the Reporting Period End Date

ERI applies—even if you sell the ETF the very next day.

Example:

- Reporting date = 31 Dec 2025

- You held the ETF on 31 Dec 2025

- You sold all holdings on 1 Jan 2026

ERI still applies.

You must:

- Declare the ERI on the Fund Distribution Date

- Add that ERI amount to your acquisition cost when calculating CGT

How ERI Reduces Future CGT

Once ERI has already been taxed, you can add it to your acquisition cost when you later sell the ETF.

This prevents double taxation.

Example

Original purchase cost = £10,000

ERI already taxed (over last 3 years) = £350

Sale proceeds = £15,000

Adjusted acquisition cost:

£10,000 + £350 = £10,350

Capital gain:

£15,000 − £10,350 = £4,650

Without adjusting for ERI, the gain would incorrectly be:

£15,000 − £10,000 = £5,000

So the ERI reduces the taxable gain by £350.

4. Dividends

Most brokers provide annual tax reports showing dividends received during the UK tax year.

Common brokers used by UK investors include:

- Trading 212

- Interactive Brokers

- Hargreaves Lansdown

These reports can normally be used when completing Self Assessment.

However, investors should check whether dividends are correctly split between:

UK Dividends

Examples:

- BP plc

- HSBC Holdings plc

These are normally UK dividends.

HMRC separates Dividends from UK companies (SA100 box 4 (Dividends from UK companies))

and Other dividends (box 5 (Other dividends)). Other dividends include dividend distributions from

authorised unit trusts, OEICs and investment trusts. If you need to split a UK payment between those

HMRC categories, you may need to check the type of instrument, because the Annual Statement does

not split them automatically.

HMRC reference: SA150 Notes, page TRG 7.

Overseas Dividends

This is where ETFs often cause confusion.

Most UCITS ETFs available to UK investors are domiciled in:

- Ireland

- Luxembourg

So ETF distributions from funds such as:

- Vanguard FTSE All-World UCITS ETF

- iShares Core MSCI World UCITS ETF

- Invesco EQQQ NASDAQ-100 UCITS ETF

are usually treated as overseas dividends for UK tax purposes, even if the ETF holds UK shares.

This is because the income is normally sourced from the country where the fund itself is domiciled, not from the countries of the underlying shares.

Some brokers clearly separate UK and overseas dividends. Others combine them, so investors may need to identify and separate them manually for Self Assessment.

Use the country, gross amount and foreign tax. If you complete SA106, use a separate row for each country and use the HMRC 3-letter country code. Do not rely on the net amount on its own. If you are using the main return for small amounts, HMRC uses SA100 box 6 (foreign dividends up to £500 – see notes) and box 7 (foreign tax taken off).

HMRC says that in limited cases, some small amounts of foreign interest and foreign dividends can go on the main return, but otherwise the Foreign pages are used. Check the current HMRC notes before filing.

HMRC reference: SA150 Notes, pages TRG 6 to TRG 7; SA106 Notes, pages FN 2 and FN 7.

Distributions

In the case of most shares and funds, these will usually be classed as dividends.

HMRC does not treat all distributions in the same way. Depending on the fund, a payment can be interest, a dividend, property income or miscellaneous income. HMRC also says reporting funds can create excess reported income, even where cash has not been paid out. Do not map the Distribution overview to one tax return box unless the tax character is clear from HMRC guidance or the fund manager information. Check HMRC HS265 or fund manager information before choosing a return box.

HMRC reference: SA150 Notes, pages TRG 6 to TRG 7; SA106 Notes, page FN 7; HS265 Offshore funds.

5. Interest on cash

HMRC uses different boxes for UK interest and foreign interest.

● UK interest: SA100 box 1 (taxed) or box 2 (untaxed).

● Foreign interest: if your only foreign income is untaxed foreign interest up to £2,000, put it in SA100 box 3 and name the country in “Any other information”.

Otherwise, use SA106.

Check the current HMRC notes before filing.

HMRC reference: SA150 Notes, page TRG 6; SA106 Notes, pages FN 6 to FN 7.

Income generated for share lending on T212 is generally counted as interest income and so can be added to any cash interest when declaring to HMRC.

Tips

For every taxable investment account outside an ISA or SIPP, keep copies of:

- Buy and sell contract notes

- Dividend statements

- ERI / Reportable Income documents

- Broker annual tax summaries

- FX conversion records for non-GBP investments

Good records make future CGT calculations much easier—especially when multiple ERI adjustments have built up over several years.

If you have several different brokers and thus several different GIAs, you should combine all trades from all brokers into one report and then calculate your taxable gains using s cslculator that follows the HMRC rules. You should NOT simply add up the gains in each broker’s annual report. First, the broker does not apply HMRC rules, and secondly, the broker does not know what other buys and sells you made in the tax year with your other brokers. To avoid errors, each tax year, you should include all the trades that you ever made frm each broker. Many people find it easier to just use one broker that has good transaction reporting for their GIA account (there is no problem using many different brokers for your ISAs, but remember the deposit limit applies across all ISA accounts!)

Many experienced UK ETF investors find that ERI tracking is one of the most commonly overlooked parts of tax reporting.

For basic-rate taxpayers, correctly declaring ERI that is taxed as dividend income, and then adding that taxed ERI to the ETF acquisition cost when you eventually sell, can reduce your overall tax bill.

This is because dividend tax for a basic-rate taxpayer is normally lower than the current 18% Capital Gains Tax rate. By declaring the ERI as a dividend when it arises, and then adding that already-taxed ERI to the ETF acquisition cost, your eventual taxable capital gain is reduced.

In effect, some of what might otherwise have been taxed later at 18% CGT is instead taxed earlier at the lower basic-rate dividend tax rate, reducing the overall tax payable.

For many investors the saving may be modest—often only £5 to £20 per year—but over many years or across multiple ETF holdings, it can add up. If you have large holdings in your GIA of accumulating ETFs, you should pay particular attention to ERI. very few CGT calculation sites include ERI in their calculations because it is very hard to automate the ERI rate lookup!